These credit reporting bureaus collect information on the balances that you owe on your debts, as well as on what kind of debts you owe. The credit reporting bureaus also obtain information on how old your accounts are, as well as whether you have paid those accounts on time or have been late. Bankruptcies, judgments against you and request for new credit are all listed on your credit report as well, and they are all factored in when deciding what your credit score should be.

What a Lender Looks At

When you decide to take a payday loan, personal loan, get a mortgage or car loan, or apply for a credit card, the lender is going to take a look at your credit score. A high credit score is going to mean that you should have an easy time getting a loan from a variety of lenders. Because you are seen as a low risk borrower if you have a high credit score, you can also expect favorable terms and a reasonable interest rate. However, a low credit score may mean that you are not going to be eligible to obtain a loan at all or that you may pay a very high premium in order to get a loan because the lender is concerned that you will not repay it on time.

Minimum Credit Scores Explained

When you apply for a personal loan, there is a minimum credit score that lenders will accept. The minimum credit score that you need in order to get a loan is going to vary based on the particular policies of the lending institution where you are seeking to borrow money. There is some variation in scoring from different credit reporting bureaus, so the ranges of scores that lenders are willing to consider is going to vary both depending upon what scoring system they use as well as depending upon how much risk the particular lender is willing to take on.

How Scoring Works

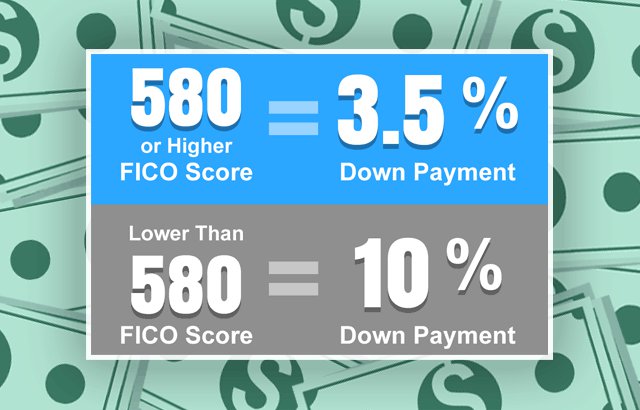

There will be some different rules for credit scores based on Vantage Scoring versus a FICO score. Typically, if a FICO score is used, a score below 580 is going to be considered an “F” Credit rating and the lender may be unwilling to give you a loan. If a Vantage score is used, then a score below 600 is likely to be considered an “F” and you are going to have a hard time finding a conventional lender who is willing to give you an unsecured loan. The scoring range for a “D” score is between 580 and 619 for a FICO scoring system and is between 600 and 699 for a Vantage scoring system. While you may be able to get a loan with a “D” score, you will probably pay a high interest rate for doing so. By the time you get into scores above around 660 for FICO or 800 for Vantage, you can expect that most lenders will give you acceptable terms for a loan. This is around where the average American’s credit score is at a 711 FICO score. If your score is above 900 for Vantage or is above 750 for FICO, you should have your pick of lenders and you should receive the most favorable loan terms.

A low score does not mean that you will never get a loan. Some lenders will be willing to look at the causes of your past credit troubles and may be willing to work with you. You should apply for a loan as soon as you need one if you have a loan score to give yourself time to find a lender who is willing to let you borrow money on reasonable terms.